Between July 3 and July 10, 2026, three things happened that had nothing to do with each other on the surface and everything to do with each other underneath. EEX reported an 11% jump in H1 2026 secondary trading volume, driven largely by financial players rotating into environmental commodities as a hedge against broader market volatility. ICE’s CORSIA futures bounced back toward $10/tonne after a volatile spring, as airlines resumed covering compliance obligations ahead of Phase I deadlines. And Macao’s new International Carbon Exchange launched standardized spot contracts for CCP-labeled technology and nature-based credit pools, signaling that even newer regional exchanges are moving straight to standardized, liquid instruments rather than one-off project listings. Read individually, these are three market news items. Read together, they say something much more specific to anyone who builds trading infrastructure: the carbon exchange matching engine sitting under most platforms today was never designed for this.

This is not a market commentary post. It’s an engineering one about the carbon exchange matching engine that has to sit underneath all three of these developments at once. If you’re a CTO, an exchange founder, or a compliance officer evaluating whether your platform’s plumbing can survive the next eighteen months of regulatory and volume shocks, the question worth asking isn’t “is the market growing.” It’s “does our carbon exchange matching engine actually behave like exchange-grade infrastructure, or does it just look like it on a demo call?”

For years, most environmental marketplaces got away with a basic database-backed order list dressed up as a carbon exchange matching engine. A seller posts a lot, a buyer submits an offer, a human or a simple script matches them, and a row gets updated. That approach was tolerable when volumes were modest, and price action was slow. It is not tolerable anymore.

The EEX volume surge is a symptom, not the disease. When secondary trading accelerates the way it did in H1 2026, order flow stops looking like occasional manual listings and starts looking like algorithmic, API-driven activity: participants hitting your endpoints repeatedly, testing spreads, and reacting to price moves in near real time. A carbon exchange matching engine built on slow, polling-based database queries simply cannot keep up. Worse, it creates exactly the kind of latency gap where stale prices get hit, orders queue unfairly, and a platform’s credibility with institutional counterparties quietly erodes trade by trade.

For any carbon exchange matching engine, the CORSIA futures recovery toward $10/tonne adds a second dimension to the same problem. Sudden regulatory price recoveries trigger bursts of compliance-driven buying from airlines racing to cover obligations, and that buying is concentrated, urgent, and unforgiving of friction. A carbon exchange matching engine that can’t distinguish a CORSIA-eligible tranche from general voluntary inventory at the moment of order placement isn’t just slow – it’s actively creating settlement risk for buyers who cannot legally clear an ineligible unit against their compliance target.

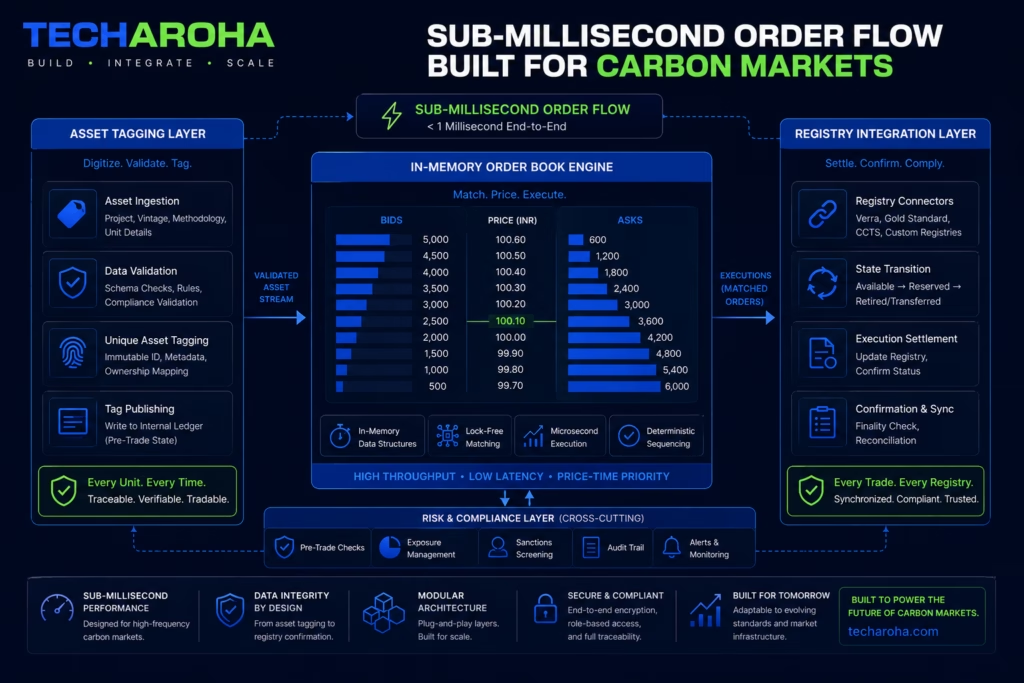

Building a carbon exchange matching engine that can absorb this kind of volume and volatility means moving off a basic relational query pattern entirely. In practice, that means a high-throughput central limit order book (CLOB) backed by an in-memory matching layer – think Redis-backed structures or a purpose-built matching service in a low-latency language – capable of resolving orders in sub-millisecond time rather than the multi-second round trips a conventional web stack produces under load.

But raw speed isn’t the whole story. A carbon exchange matching engine handling CORSIA-eligible inventory needs specialized asset tagging baked into the order book itself, not bolted on as a front-end filter. Compliance buyers need to query and clear against CORSIA-eligible tranches specifically, instantly, without wading through a mixed pool of voluntary and compliance-grade units during a volatile trading window. That tagging has to live at the data layer the matching engine reads from – because a filter that only exists in the UI does nothing to stop an API call, a race condition, or an internal override from clearing a trade the buyer legally cannot accept.

This is the part most legacy platforms miss: a carbon exchange matching engine isn’t just an order-matching component. It’s the single point in your architecture where speed, eligibility, and legal state all have to reconcile in the same instant, because a trade that clears fast but clears wrong is worse than a trade that clears slowly.

Read our latest article about Cryptographic Proofs vs. PDF Uploads: Eliminating Letter of Authorization (LoA) Counterparty Risk in Compliance Trading

The UNFCCC’s announcement that foundational Article 6 registries will be fully operational by year-end changes what a carbon exchange matching engine has to talk to, not just how fast it has to talk. Once sovereign state ledgers go live, platforms need an asynchronous Registry Integration Layer built on durable webhooks and automated reconciliation queues – infrastructure that can absorb a national registry’s own timeline for issuing corresponding adjustments without stalling the matching engine itself. A carbon exchange matching engine that waits synchronously on a sovereign registry response is a matching engine that will eventually time out during exactly the compliance rush it needs to survive.

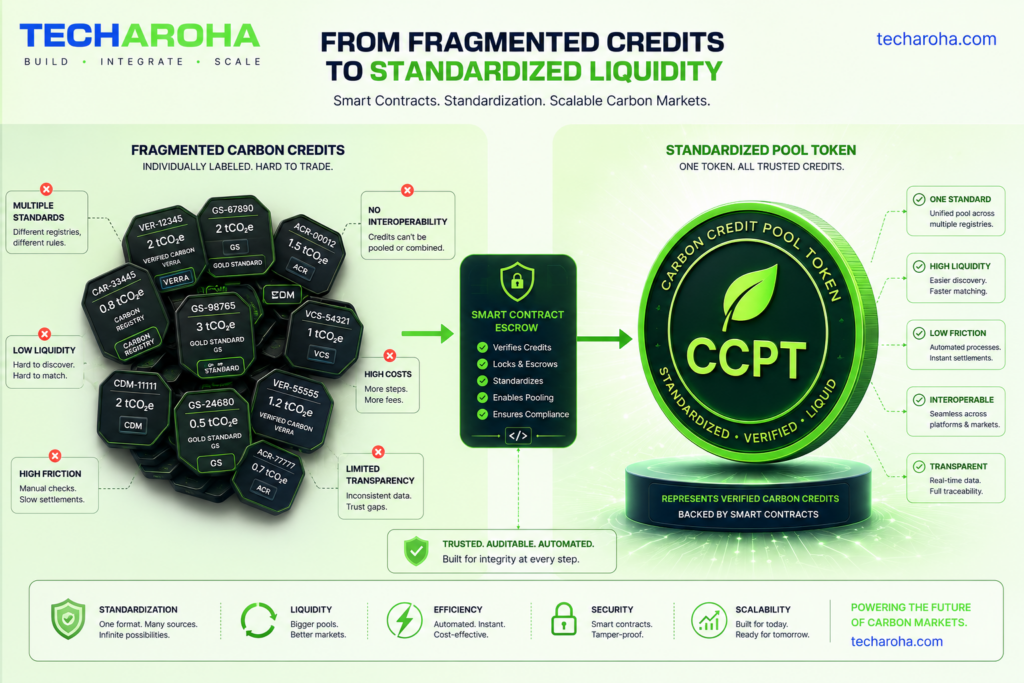

Macao’s move toward standardized CCP-labeled spot contracts points at a related but distinct requirement: pooling. Heterogeneous, project-specific credits need to be lockable into escrow and re-minted as a uniform, tradable pool token – a Tech-CCP or Nature-CCP equivalent- so a carbon exchange matching engine can offer the deep, standardized liquidity institutional desks actually want, instead of forcing every buyer to underwrite project-level risk on every single lot. This is the exact problem NFT and blockchain-backed exchange infrastructure was built to solve: each underlying credit is minted as a traceable NFT, lockable into an escrow contract that issues a standardized pool token on top, so a carbon exchange matching engine can trade the pool as one liquid instrument while still tracing every unit back to its originating project on-chain.

The European Commission’s draft €6 billion overhaul extending EU ETS free allowance timelines into the 2040s a move aimed at cushioning heavy industry from the full cost of decarbonization while it retools is the clearest possible illustration of a principle every carbon exchange matching engine has to be built around: compliance parameters change, sometimes by billions of euros and multiple decades, and your core trading logic cannot be the thing that breaks when they do.

If allowance expiration windows, allocation quotas, and cross-border adjustment rules are hardcoded into the same codebase that runs your carbon exchange matching engine, a regulatory overhaul like this one forces a full redeploy of your most critical system under time pressure. That’s an unacceptable risk profile for anything calling itself exchange-grade. The fix is a decoupled Compliance & Rules Engine – a separate, dynamically configurable microservice that the carbon exchange matching engine queries at the moment of order validation, rather than a set of assumptions baked into the matching logic itself. When the next multi-billion-euro overhaul lands, and it will, you update rule parameters in a service designed to change, not the low-latency core that can’t afford to.

If you’re a CTO or exchange founder reading the July 2026 headlines, the honest diagnostic questions are these:

Most platforms built in the last several years can answer yes to maybe one of those. The news from early July makes clear the market won’t wait for the rest to catch up.

Techaroha builds NFT and blockchain-backed Carbon Trading Exchange platforms and Carbon Registries engineered for exactly this kind of volume, volatility, and regulatory change. Let’s con