A compliance buyer at an international airline opens your platform, filters for Article 6.4-eligible inventory, and clears an order against a lot of what your database calls “available credits.” Forty minutes later, the host country’s national authority issues a Letter of Authorization on a completely unrelated administrative timeline, and the units the airline just bought quietly stop being what they were sold as. The row in your ledger didn’t change. The legal reality underneath it did. This is not a hypothetical edge case dreamed up for a conference panel. It is the structural consequence of how the Paris Agreement Crediting Mechanism (PACM) actually works, and it is the single most under-engineered problem in carbon market software right now. Any platform still treating credits as flat, static rows is building on a foundation that the regulation itself has already made obsolete. What every serious exchange, registry, and compliance desk needs instead is a carbon credit state machine architecture, and almost nobody has one. Why a Single Credit Now Has Two Legal Identities Under Article 6.4, a project doesn’t just issue “carbon credits.” It issues Article 6.4 Emission Reductions, or A6.4ERs, and those units arrive in one of two legal states. If the host country has not authorized a unit for international use, it is issued and held as a Mitigation Contribution Unit (MCU) usable domestically, for results-based climate finance, or for a country’s own NDC, but legally barred from crossing a border for compliance purposes. If the host country has authorized the unit and applied a corresponding adjustment, it becomes an Authorized Emission Reduction (AER), eligible to move internationally and clear against schemes like CORSIA. Here is the part that breaks flat databases: a unit issued as an MCU is not permanently an MCU. Host countries can grant retroactive authorization, and the moment they do, that unit’s legal identity flips – it stops being a domestically-contained MCU and becomes an internationally transferable AER, provided it hasn’t already been transferred out of the mechanism registry. The reverse containment rule matters just as much: MCUs remain confined to transactions within the mechanism registry until that authorization event happens. A platform’s asset ledger is not looking at one static object. It’s looking at a unit with a lifecycle, governed by a decision made by a national authority on a timeline your engineering team does not control and often can’t even observe in real time. This is exactly why a carbon credit state machine architecture has to be the starting assumption for any exchange handling Article 6.4 inventory, not a feature bolted on after the first compliance incident. The Structural Problem: What Happens When Your Ledger Treats Credits as Fungible Rows Picture the default approach most platforms take, because it’s the same approach that has worked fine for years of pre-Article-6 voluntary credits: a table with a credit ID, a project reference, a vintage, a quantity, and a status column that says “available,” “retired,” or “sold.” Fungible. Flat. Fast to query. Now put an MCU into that table. The status column says “available.” A compliance buyer, say, an airline covering CORSIA obligations – filters inventory, sees the lot, and clears the trade. Nothing in the schema stopped this, because nothing in the schema knew the difference between an MCU and an AER in the first place. The airline has now taken legal ownership of a unit that cannot clear their compliance ledger, because it was never authorized for international transfer at the moment of sale. Nobody committed fraud. The seller may not have even realized the lot hadn’t cleared host-country authorization. The matching engine did exactly what matching engines do: it matched a buy order against available inventory. The failure isn’t behavioral. It’s architectural. A platform without a carbon credit state machine architecture cannot distinguish between an MCU and an AER at the only moment that legally matters: the instant before settlement, because it was never built to track legal state as a first-class property of the asset. This is the exact failure mode regulators are now scrutinizing under anti-greenwashing enforcement regimes. It’s not enough to detect the mismatch after the fact through a reconciliation job. The question examiners are asking exchange operators is whether the platform’s data model made an unauthorized clearing possible in the first place. If the answer is yes, that’s not a footnote. That’s an exposure line item with a compliance buyer’s name attached to it. The Software Architecture Solution: A Conditional State-Machine Pattern for the Asset Ledger The fix is not a better compliance checkbox, and it’s not a nightly reconciliation batch that tells you about a mismatch twelve hours after it already cleared. The fix is redesigning the asset ledger so that a unit’s authorization status is a governed state, not a display label. This is the core of a functioning carbon credit state machine architecture. Here’s the shape of it, stripped to its engineering bones. Why “Just Add a Status Filter” Doesn’t Solve This The tempting shortcut here is the same one platforms reached for with dual-claiming risk: add a filter on the front end so buyers “should” only see eligible inventory, and add an attestation checkbox at checkout confirming the buyer understands the unit’s authorization status. This does almost nothing, for the same reason it never works elsewhere. A front-end filter is a display convenience, not an architectural guarantee; it doesn’t stop an API call, an internal admin override, or a race condition where a unit’s status changes between page load and order submission from clearing an ineligible trade anyway. An attestation checkbox shifts liability onto a buyer’s understanding of a UN mechanism most corporate procurement teams have never had to parse line by line. Neither approach constitutes a carbon credit state machine architecture. Both are policy dressed up as engineering, and regulators evaluating anti-greenwashing controls are no longer satisfied by the distinction between “we tell the buyer” and “we structurally prevent the mismatch.” They’re asking whether the platform’s asset ledger could have allowed this trade

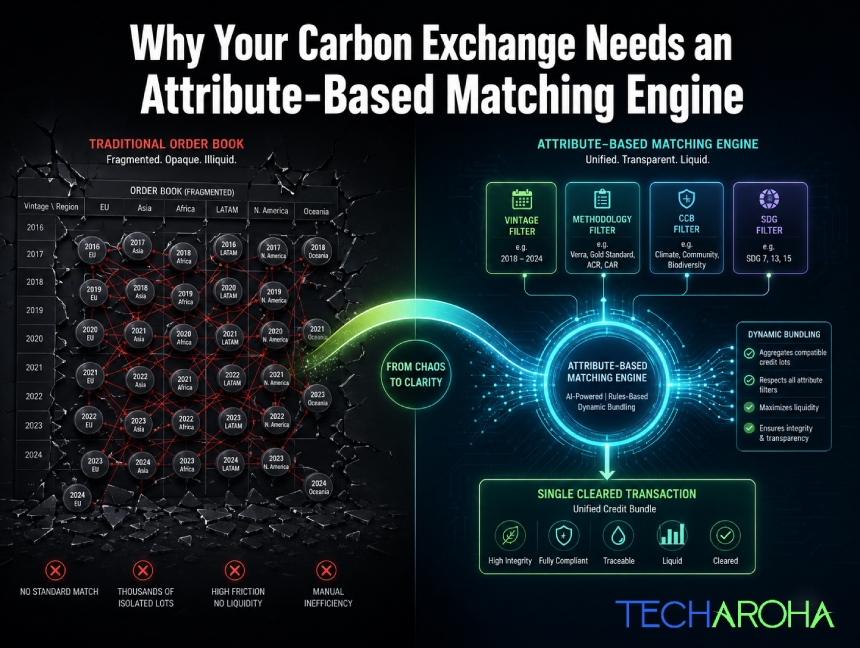

The trading infrastructure built for stocks and Bitcoin will systematically destroy liquidity in any carbon exchange. Here is the architectural fix and the exact engineering logic behind it. Carbon markets are at an inflection point. Voluntary carbon credit issuances have grown into a multi-hundred-billion-dollar projected market, institutional buyers are entering at scale, and Article 6.4 is formalizing cross-border credit flows in ways that would have seemed theoretical five years ago. Exchange founders are raising capital. Trading desks are staffing up. And almost every single one of them is about to make the same catastrophic infrastructure mistake. They are going to build a Central Limit Order Book (CLOB). The CLOB is the gold standard of financial exchange architecture. It powers the NYSE. It underpins every top-tier crypto exchange. It is fast, transparent, price-time priority-driven, and battle-tested. For carbon credits, it is the wrong tool in precisely the way that a pneumatic drill is the wrong tool for a surgical procedure. Not ineffective in general. Lethally ineffective here. This article is a precise technical and economic explanation of why, and a blueprint for the architecture that actually works: the carbon credit trading platform matching engine built on attribute-indexed, parameter-based order resolution. If you are building or operating a carbon exchange, a carbon trading desk, or evaluating infrastructure for a voluntary carbon market platform, this is the engineering decision that will determine whether your liquidity pool deepens or evaporates. Part 1: Why the CLOB Destroys Carbon Liquidity – The Structural Problem A Central Limit Order Book works on one foundational assumption: The asset is fungible. One share of AAPL is identical to every other share of AAPL. One Bitcoin is identical to every other Bitcoin. The order book can aggregate all bids and all asks into a single depth ladder because every unit on both sides of the book represents the same underlying thing. Carbon credits are not the same underlying thing. A 2021 cookstove credit from a Gold Standard-certified project in rural Kenya and a 2025 direct-air-capture credit from a Climeworks facility in Iceland are both “one tonne of CO₂ equivalent.” That is where the similarity ends.They have different: And, critically, they clear at prices that can differ by a factor of 10 or more. Institutional buyers do not treat them as interchangeable. Compliance frameworks do not treat them as interchangeable. Even voluntary corporate buyers with qualitative net-zero targets frequently cannot treat them as interchangeable without triggering greenwashing liability. What Happens When You Force Carbon Credits Into a CLOB? The matching engine identifies the asset by symbol. To maintain the fiction of fungibility across radically different credits, you have only two options: In a mature carbon market with: …you end up with thousands of discrete order books. Each one is individually empty. A liquidity pool that should be $50 million deep becomes: The consequences are predictable: The platform appears broken because, functionally, it is. This is not hypothetical. It is exactly why the voluntary carbon market spent years operating primarily as an OTC market conducted through brokers and phone calls. The asset’s heterogeneity made exchange-style infrastructure practically non-functional for real trading.A carbon credit trading platform matching engine that copies traditional financial exchange architecture without accounting for this reality will simply recreate that illiquidity problem at scale. Part 2: The Right Architecture – Attribute-Based Matching Over an Indexed Credit Graph The correct mental model for a carbon exchange is not a stock exchange. It is closer to a parametric procurement engine. The kind of system that allows a large corporate buyer to issue a single tender specification (“supply 10,000 units of this type of component, meeting these tolerances, at under this price”) and have the system dynamically identify, aggregate, and clear supply from multiple disparate sources to fulfill the single order. Applied to carbon, the architecture has three layers. Layer 1: The Credit Attribute Graph (Transactional Database) Every credit lot is stored as a structured object with a rich attribute schema not merely a quantity and price.A credit record contains: This is a normalized relational schema in your primary transactional database. PostgreSQL is an appropriate choice for ACID compliance on settlements. But the transactional database alone cannot power real-time matching at query complexity levels that carbon requires. Write about our blog that explains- The Ghost Credit Trap: What No One Tells You About Carbon Registry API Integration Layer 2: The Attribute Index (Elasticsearch or Redis Search) This is the layer many platforms either skip or implement incorrectly. The carbon credit trading platform matching engine requires a secondary search index optimized for: Elasticsearch Advantages Redis Search Advantages For institutional-scale exchanges, a hybrid architecture makes sense: Example Redis Search Schema With this index in place, the matching engine can execute parametric queries in real time. A buyer placing an order like “Buy 10,000 tonnes of any Nature-Based Removal, vintage 2023 or later, CCB certified, under $18 per tonne” translates directly to an indexed query: Example Buyer Query Buyer requests: Buy 10,000 tonnes of any Nature-Based Removal, vintage 2023+, CCB certified, under $18/tonne. This query executes against the in-memory index in under 5 milliseconds and returns every matching available lot ranked by price, regardless of which project, geography, or vintage within the buyer’s specification each lot originates from. Layer 3: The Dynamic Bundling and Clearing Algorithm The search query returns a ranked list of available lots. The matching engine’s clearing algorithm then executes a greedy fulfillment sweep: The buyer receives a single trade confirmation -10,000 tonnes cleared at a volume-weighted average price of $16.43/tonne across 7 credit lots, not 7 individual trade notifications across 7 empty order books. The seller-side experience is equally clean: individual lot holders have their available inventory consumed by the engine, with settlement proceeds routed per standard clearing logic. This is the structural breakthrough. The carbon credit trading platform matching engine does not require both sides to agree on a specific lot. It requires only that a buyer’s parameter specification encompasses the seller’s lot attributes. The parameter space is the order

The world’s race to decarbonize its economy has never needed carbon markets more. More than 28% of global emissions fall under a carbon price as of 2025 and voluntary markets reached a half-year high of 95 million carbon credit retirements in the first six months of the year. Demand is there, but scrutiny is even more so — buyers want to know that every credit they purchase actually reflects a genuine and unique reduction in emissions. At the core of this is a series of carbon registries, the official record-keepers of issuance, transfer and retirement of credits. They have always been the trusted “source of truth.” But as markets grow in scale and digitize, blockchain-based systems are arriving to supplement them — offering transparency, programmability, and efficiency. The question isn’t whether blockchain will replace registries (it won’t), but how the two might coexist to enhance trust and efficiency. This blog explores what traditional registries like Verra or Gold Standard offer in comparison to blockchain platforms, and the pros, cons, and risks of bringing the two together. We’ll also consider recent developments, such as India’s Carbon Credit Trading Scheme, and the growing popularity of high-integrity credits — before we answer the questions on the lips of businesses and investors in 2025. A quick primer: what a carbon registry actually does A carbon registry functions as the central, immutable ledger for carbon credits, assigning each one a serial number and accompanying documentation that proves its origins and lifespan. These ledgers are the assurance that buyers can check to prevent the risk of double-counting, and they confirm the approved methodology, the lineage of ownership, and that a credit has been permanently retired. The largest registries at present are Verra, operating under its Verified Carbon Standard (VCS), and Gold Standard. Why this matters in 2025: The carbon market is systematically prioritising “high-integrity” credits. Assessments of additionality, permanence, leakage and the formal consent of the host country, as mandated under the Article 6 framework of the Paris Agreement, have become increasingly stringent. Registry metadata and on-label indicators are thus being enhanced to allow purchasers to filter and evaluate credit quality before committing capital. Where blockchain fits (and where it doesn’t) What blockchain adds (when done right): Tamper-evident audit trails. Tamper-evident audit trails. Such on-chain records can potentially be used to trace all credit movement and every loan, with links to the serials on the registry and to the documents proving verification. Programmability. With smart contracts, escrow, dvp, retire-on-evidence milestones can all be automated (e.g., IOT/satellite proof on nature projects). Interoperability & liquidity. Tokens can be used to represent claims, make it possible for fractional ownership and create secondary markets – subject to the condition that the token is cryptographically bound to the originating serial and retirement status. Each carbon credit can be represented as a unique NFT (non-fungible token), meaning that just as every registry-issued credit has a distinct serial number, its on-chain version can be minted as an NFT with embedded metadata (project ID, methodology, MRV hashes). This ensures 1:1 traceability between the registry unit and the blockchain representation. Limits & Risks: (lessons from 2021–2024): What’s new in 2025 (and why it changes the calculus) Risks to Monitor Duplicate tokens: A credit token lacking a current registry serial may be erroneously repeated. Weak methodologies: Blockchain can’t fix poor additionality or permanence—it just records data.Regulatory drift: Regulatory texts (e.g. Article 6, CCTS) evolve, requiring adaptive technical designs. Liquidity vs. quality: Markets are prioritizing integrity over speculation in 2025. Pros & Cons: Side-by-Side Aspect Traditional Registries Blockchain Layers Trust Accepted by regulators, airlines, and corporations. Adds transparency if linked properly; otherwise creates risk. Data Comprehensive but siloed, sometimes slow to update. Open, real-time records accessible globally. Efficiency Manual processes, limited automation. Smart contracts automate transfers and settlements. Risk Low, as long as registry governance holds. High if tokens are unbacked or duplicated. How they work together (the practical stack) Blueprint for 2025 infrastructures, suitable for both developers and buyers: Origin within a recognized registry (Verra or Gold Standard). Treat the registry as the definitive source for serials, holder data, and retirement events. The registry retains primacy. Create a permissioned, append-only on-chain replica, recording serials, approved methodology IDs, and hashes from the validation report. Frame tokens within strict boundaries: Leverage programmable contracts for delivery-versus-payment, escrow, and milestone releases—especially suited for nature-based projects with staged verification. Publish quality metadata—new GS labels and risk ratings—directly on-chain. This enables buyers to filter by integrity before executing transactions. Concrete signals in India: Both public and private sectors are advancing carbon-credit infrastructure, from regionally mandated carbon banks on Hedera to NABARD’s on-farm pilots. Growing demand is anticipated for digital MRV and interoperable slugs that externally settle while still keyed to the on-chart registry. Real-world examples (2025) Quick buyer checklist (2025) Bottom line Always treat the Verra and Gold Standard registries as authoritative for issuance, ownership, and retirement. Use the blockchain as an additive, not as an alternative, channel for transparent and automated processes—registry governance remains sovereign. NFT structures make sense only when each NFT directly mirrors a registry serial; without that link, they become shadow assets. Implement a 1:1 token-to-serial linkage with automated on-chain burn triggered by registry retirement, designed expressly to avert double counting. Synchronize with CCTS, CORSIA, Article 6 provisions, and the latest registry tags. The threshold for integrity is trending upwards, and 2025 data is already showing that buyers are steering toward supply that is evidently higher quality. FAQs Which is “better”: blockchain or traditional registries?Neither stands alone. Registries confer authority; blockchain brings speed and traceability. Can I make valid climate claims with just a token?No. Claims depend on a registry retirement (and any Article 6 or CORSIA stipulations). Tokens must cite those retirements. What statistics define 2025’s market?About 28% of emissions will sit under a carbon-priced system; retirements will hit 95 million in the first half of 2025—a record for any half. Does India’s CCTS allow tokenized trading?CCTS lays out compliance frameworks and targets; token frameworks must