The 2026 Signal You Cannot Ignore The first half of 2026 handed the voluntary carbon market a statistic that reframes everything: credit retirements — actual, verified demand from corporate buyers — hit an all-time record high, while global issuances dropped by 44% compared to the same period in 2025, according to AlliedOffsets data. Read that twice. Demand is at its peak. Supply is collapsing. This is not a temporary correction. High-integrity spot credits take years to develop, verify, and issue. The pipeline that produces them is structurally constrained, and no amount of buyer appetite can compress that timeline. What buyers — and the platforms serving them — are doing instead is moving aggressively into forward offtake agreements: locking in future vintage deliveries today, often before a project has issued a single credit, in exchange for upfront or milestone-linked capital. For platform builders and exchange operators, this shift carries a hard technical consequence. The infrastructure required to operate a carbon forward contract platform is fundamentally different from a spot trading engine. The two are not just different in scale. They are different in kind. Spot Infrastructure Is the Wrong Foundation A spot trade engine is conceptually straightforward. A buyer submits a purchase order, the system matches it against available inventory, the registry API confirms the serial transfer, and the credit is retired. Settlement is near-instantaneous. Risk is bounded at the transaction level. The engine does not need to care about what happens in three years. A carbon forward contract platform cannot inherit that architecture. Every assumption changes. Delivery is deferred — sometimes by five to ten years. The project that will produce the credits may not yet have completed its first verification cycle. Pricing may be fixed at signing but subject to quality adjustment clauses tied to co-benefit outcomes. Capital may flow in tranches, not as a lump sum. Default scenarios — what happens if the project underperforms, misses a verification window, or suffers a reversal event — must be encoded, not handled manually. Any development team that attempts to build forward contract infrastructure on top of a spot matching engine will hit structural limits within the first contract cycle. The data model, the state machine, and the risk management layer all need to be purpose-built. What a Carbon Forward Contract Platform Actually Needs to Do Before writing a line of code, it is worth being precise about the functional envelope a carbon forward contract platform must cover. These are not nice-to-have features. They are the baseline required to make a forward offtake agreement enforceable and auditable on a digital platform. Engineering the Milestone Escrow Module The technical core of a carbon forward contract platform is the milestone escrow module. This is where structured finance meets programmable infrastructure. The design pattern works as follows. At contract execution, the buyer’s capital commitment is moved into a permissioned escrow state — either via a smart contract on a compatible ledger (EVM-compatible chains, Hyperledger Fabric, or permissioned Hedera environments have all been used in production carbon infrastructure) or via a custodied fiat escrow account managed by the platform’s treasury layer, depending on regulatory context. The capital does not move again until a milestone condition is satisfied. Each milestone is defined in the contract as a structured data object containing three fields: the event type (e.g., “initial biomass verification”), the verification source (e.g., a named third-party auditor or a specific satellite data feed), and the release amount (the capital tranche to be unlocked on confirmation). The platform’s milestone engine polls the verification source, receives a signed confirmation event, cross-references it against the contract’s milestone schedule, and if the condition is met, initiates the capital release to the project developer’s account. The critical design decision here is the oracle architecture. dMRV data does not arrive in a form that a contract engine can consume directly. Satellite imagery needs to be parsed into standardized biomass delta signals. IoT sensor aggregates need to be normalized and signed by a trusted verification node before they can trigger a financial event. A well-built carbon forward contract platform includes a dMRV oracle layer that transforms raw monitoring data into signed, timestamped attestation events that the escrow engine can resolve against. For nature-based projects, the milestone sequence typically runs: independent validation → first monitoring report → initial credit issuance confirmation. For engineered removals — biochar, enhanced rock weathering, direct air capture — the milestone triggers are more granular: feedstock tonnage confirmation, operational capacity certification, and then periodic tonne-verified issuance against the contracted volume. Default Buffers and Non-Delivery Risk A carbon forward contract platform that does not encode default handling is not a platform. It is a promissory note management system. Default scenarios are not edge cases in forward carbon markets — project timelines slip, verification bodies discover discrepancies, and force majeure events affect land-based projects routinely. The engineering solution is a two-layer default architecture. The first layer is the delivery buffer. At contract inception, the platform locks a percentage of the project’s expected issuance volume — typically 10 to 20 percent — into a buffer account. This buffer is denominated in anticipated credits, not capital, and is managed via a registry subaccount or an on-chain token reserve, depending on the platform’s issuance model. If the project delivers short in any given vintage year, the platform automatically draws from the buffer to fulfill the buyer’s contract position. The second layer is the capital clawback mechanism. If the buffer is exhausted and the project remains in default — delivery shortfall exceeds the buffer reserve within a defined cure period — the platform enforces a partial or full capital recovery against the remaining escrow balance. This requires the contract to define a clear priority waterfall: what portion of the undeployed escrow reverts to the buyer, what portion is forfeited, and under what conditions the developer retains any remainder. The state machine for this layer needs to be auditable. Every state transition — from active to in-default, from buffer-drawn to clawback-initiated — must produce a

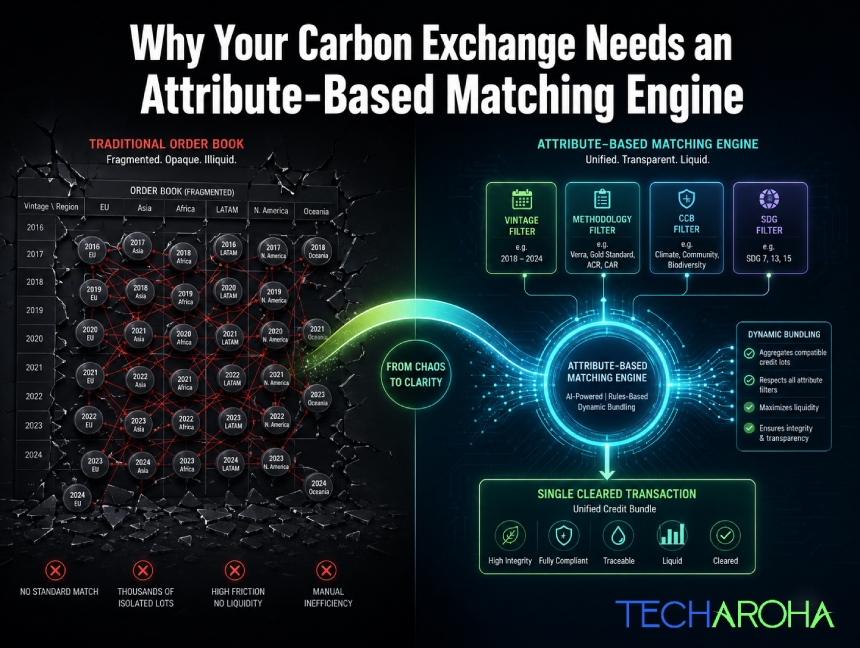

The trading infrastructure built for stocks and Bitcoin will systematically destroy liquidity in any carbon exchange. Here is the architectural fix and the exact engineering logic behind it. Carbon markets are at an inflection point. Voluntary carbon credit issuances have grown into a multi-hundred-billion-dollar projected market, institutional buyers are entering at scale, and Article 6.4 is formalizing cross-border credit flows in ways that would have seemed theoretical five years ago. Exchange founders are raising capital. Trading desks are staffing up. And almost every single one of them is about to make the same catastrophic infrastructure mistake. They are going to build a Central Limit Order Book (CLOB). The CLOB is the gold standard of financial exchange architecture. It powers the NYSE. It underpins every top-tier crypto exchange. It is fast, transparent, price-time priority-driven, and battle-tested. For carbon credits, it is the wrong tool in precisely the way that a pneumatic drill is the wrong tool for a surgical procedure. Not ineffective in general. Lethally ineffective here. This article is a precise technical and economic explanation of why, and a blueprint for the architecture that actually works: the carbon credit trading platform matching engine built on attribute-indexed, parameter-based order resolution. If you are building or operating a carbon exchange, a carbon trading desk, or evaluating infrastructure for a voluntary carbon market platform, this is the engineering decision that will determine whether your liquidity pool deepens or evaporates. Part 1: Why the CLOB Destroys Carbon Liquidity – The Structural Problem A Central Limit Order Book works on one foundational assumption: The asset is fungible. One share of AAPL is identical to every other share of AAPL. One Bitcoin is identical to every other Bitcoin. The order book can aggregate all bids and all asks into a single depth ladder because every unit on both sides of the book represents the same underlying thing. Carbon credits are not the same underlying thing. A 2021 cookstove credit from a Gold Standard-certified project in rural Kenya and a 2025 direct-air-capture credit from a Climeworks facility in Iceland are both “one tonne of CO₂ equivalent.” That is where the similarity ends.They have different: And, critically, they clear at prices that can differ by a factor of 10 or more. Institutional buyers do not treat them as interchangeable. Compliance frameworks do not treat them as interchangeable. Even voluntary corporate buyers with qualitative net-zero targets frequently cannot treat them as interchangeable without triggering greenwashing liability. What Happens When You Force Carbon Credits Into a CLOB? The matching engine identifies the asset by symbol. To maintain the fiction of fungibility across radically different credits, you have only two options: In a mature carbon market with: …you end up with thousands of discrete order books. Each one is individually empty. A liquidity pool that should be $50 million deep becomes: The consequences are predictable: The platform appears broken because, functionally, it is. This is not hypothetical. It is exactly why the voluntary carbon market spent years operating primarily as an OTC market conducted through brokers and phone calls. The asset’s heterogeneity made exchange-style infrastructure practically non-functional for real trading.A carbon credit trading platform matching engine that copies traditional financial exchange architecture without accounting for this reality will simply recreate that illiquidity problem at scale. Part 2: The Right Architecture – Attribute-Based Matching Over an Indexed Credit Graph The correct mental model for a carbon exchange is not a stock exchange. It is closer to a parametric procurement engine. The kind of system that allows a large corporate buyer to issue a single tender specification (“supply 10,000 units of this type of component, meeting these tolerances, at under this price”) and have the system dynamically identify, aggregate, and clear supply from multiple disparate sources to fulfill the single order. Applied to carbon, the architecture has three layers. Layer 1: The Credit Attribute Graph (Transactional Database) Every credit lot is stored as a structured object with a rich attribute schema not merely a quantity and price.A credit record contains: This is a normalized relational schema in your primary transactional database. PostgreSQL is an appropriate choice for ACID compliance on settlements. But the transactional database alone cannot power real-time matching at query complexity levels that carbon requires. Write about our blog that explains- The Ghost Credit Trap: What No One Tells You About Carbon Registry API Integration Layer 2: The Attribute Index (Elasticsearch or Redis Search) This is the layer many platforms either skip or implement incorrectly. The carbon credit trading platform matching engine requires a secondary search index optimized for: Elasticsearch Advantages Redis Search Advantages For institutional-scale exchanges, a hybrid architecture makes sense: Example Redis Search Schema With this index in place, the matching engine can execute parametric queries in real time. A buyer placing an order like “Buy 10,000 tonnes of any Nature-Based Removal, vintage 2023 or later, CCB certified, under $18 per tonne” translates directly to an indexed query: Example Buyer Query Buyer requests: Buy 10,000 tonnes of any Nature-Based Removal, vintage 2023+, CCB certified, under $18/tonne. This query executes against the in-memory index in under 5 milliseconds and returns every matching available lot ranked by price, regardless of which project, geography, or vintage within the buyer’s specification each lot originates from. Layer 3: The Dynamic Bundling and Clearing Algorithm The search query returns a ranked list of available lots. The matching engine’s clearing algorithm then executes a greedy fulfillment sweep: The buyer receives a single trade confirmation -10,000 tonnes cleared at a volume-weighted average price of $16.43/tonne across 7 credit lots, not 7 individual trade notifications across 7 empty order books. The seller-side experience is equally clean: individual lot holders have their available inventory consumed by the engine, with settlement proceeds routed per standard clearing logic. This is the structural breakthrough. The carbon credit trading platform matching engine does not require both sides to agree on a specific lot. It requires only that a buyer’s parameter specification encompasses the seller’s lot attributes. The parameter space is the order

Carbon credit management platform infrastructure is becoming the backbone of a rapidly expanding global carbon market. As voluntary carbon markets surpass $2 billion annually and compliance schemes accelerate across India, Europe, Japan, and Singapore, the industry faces a growing challenge: operational scalability. Beyond concerns about credit integrity, outdated processes, manual workflows, and verification bottlenecks are creating costly inefficiencies that could erase billions in market value, making modern carbon market infrastructure more critical than ever. This blog identifies six specific operational bottlenecks that break carbon credit management platforms at the point that matters most: after a deal has been agreed, before the value is delivered. If you are building, operating, or commissioning a platform for the carbon market, these are the failure points your architecture needs to address by design. Bottleneck 1: Credit State Synchronization Lag Every carbon credit management platform maintains an internal representation of credit status: available, reserved, transferred, retired. The problem is that this internal state and the registry’s confirmed state are almost never in sync. When a buyer initiates a purchase, the platform marks the credit as “reserved.” But the underlying registry — Verra, Gold Standard, India’s Grid Controller CCC registry — has not confirmed the transfer yet. That confirmation window can stretch from hours to days depending on the registry’s processing schedule and batch synchronization cycle. In securities markets, clearinghouses enforce T+2 settlement cycles. Carbon markets have no equivalent standard, with OTC bilateral trades routinely settling on T+5 to T+30 timelines. For a corporate buyer claiming carbon neutrality for a reporting period, a multi-day status ambiguity is not merely inconvenient. It is a compliance exposure. If the credit status reads “reserved but unconfirmed” at a reporting deadline, the underlying climate claim is technically unsupported. A purpose-built carbon credit management platform addresses this through event-driven registry synchronization: webhook listeners to registry APIs that reflect confirmed state changes in near real-time, rather than batch-syncing on a 24-hour schedule. This alone compresses the synchronization window from days to minutes. Bottleneck 2: MRV Data Ingestion Delays Measurement, Reporting, and Verification is the legitimacy foundation of every carbon credit. It is also where most carbon credit management platforms quietly collapse under operational load. MRV data arrives from inconsistent sources: IoT sensors on industrial equipment, satellite deforestation analysis feeds, field agent reports in PDF format, third-party verifier spreadsheets, and manual laboratory results. Each source has different formatting, frequency, and unit conventions. Most platforms receive this data and process it manually — a compliance officer downloads a file, reformats it, and uploads it to a registry-submission template. Thallo’s research found that eliminating unnecessary verification wait times could double the speed of credit issuance. The constraint is rarely the verifier’s judgment. It is the time cost of assembling, normalizing, and submitting heterogeneous data. An operationally mature carbon credit management platform replaces this manual pipeline with an automated MRV ingestion engine: a structured data layer that accepts multiple input formats via API, CSV, or OCR-extracted PDF, normalizes against approved emission factor libraries, and auto-generates pre-filled registry submission drafts. Verification reviewers work from structured packages rather than raw field exports. This alone can compress verification cycles from six weeks to two — without reducing regulatory rigor. Bottleneck 3: Counterparty Onboarding Friction New participants joining a carbon credit management platform must pass KYC/AML screening, project eligibility verification, and registry credential linkage before they can transact. For compliance markets, these checks are mandatory. For the voluntary carbon market, they are increasingly expected by institutional buyers. The operational failure is in implementation. Most platforms run these checks manually through compliance teams using separate systems that do not connect to the trading layer. A corporate buyer wanting to acquire BECCS credits may wait four to eight weeks for account activation — during which the available credits are purchased by another buyer, and the deal that was ready to close does not. This is an integration architecture problem, not a regulatory one. Embedding KYC/AML API workflows directly into the onboarding flow — with automated document verification, sanctions screening, and registry credential provisioning — compresses the onboarding cycle from weeks to days without reducing due diligence standards. For operators wanting to serve institutional counterparties at scale, onboarding velocity is a direct revenue variable. Bottleneck 4: Settlement Without Programmatic Escrow The most under-discussed structural risk in carbon trading is counterparty exposure — the risk that one party to a bilateral deal fails to deliver after the other has committed. In securities markets, central clearing manages this risk. In most carbon markets, it is managed by contract, phone calls, and trust. Most carbon credit management platforms lack native escrow-and-release logic. When a buyer agrees to purchase verified emission reductions at a fixed price, the platform records the agreement. But the actual mechanics of delivery — payment confirmation, credit transfer trigger, registry retirement confirmation — are executed manually by operations teams on both sides. This creates simultaneous dual exposure. The buyer has paid but cannot confirm delivery until the registry reflects the transfer. The seller has transferred credits but cannot confirm payment until bank settlement clears. A carbon credit management platform with programmatic escrow eliminates both exposures through an atomic swap: funds are locked in escrow at trade agreement, credits are held in a platform-controlled staging account, and both are released simultaneously only when both confirmation conditions are satisfied. This is not sophisticated financial engineering. It is standard financial infrastructure logic applied to a market that has not historically demanded it — until institutional capital began entering carbon markets and bringing institutional risk standards with it. Bottleneck 5: Credit Lifecycle Custody Fragmentation A carbon credit does not simply exist at a fixed address. It moves — from registry issuance through a developer account, through broker inventory, into a buyer’s holding account, through optional secondary transfers, and finally into retirement. Each step changes custody. Each custody change should be atomically recorded. In practice, most carbon credit management platforms track custody state across parallel silos: the platform database holds one version, the registry holds another (typically

On the morning of March 26, 2026, Brent crude crossed $107 a barrel. Oil traders held their breath. CFOs across every energy-intensive sector scrambled to recalculate Q2 forecasts. And somewhere in the noise, a quieter, more consequential question surfaced one that most boardrooms are not yet asking: What does $100+ oil mean for carbon credit trading platform development? The answer is counterintuitive, commercially significant, and for the businesses reading this, time-sensitive. The Paradox Nobody Is Talking About Wars are terrible for short-term climate investment. Nobody disputes that. When the US-Israel strikes on Iran disrupted the Strait of Hormuz, and Brent surged 15% overnight, the initial narrative was predictable: energy security over climate ambition, fossil fuels back in the spotlight, green transition on pause. But history disagrees with that narrative – and the data from the last three weeks of trading confirms it. The same pattern played out in 2022 when Russia invaded Ukraine. Oil spiked. LNG markets fractured. Governments that had been drifting on clean energy suddenly found religion, not because they had a moral awakening, but because energy independence became the most urgent national security issue on the table. Europe deployed renewables at record speed. Solar and wind installations accelerated. And carbon markets? They expanded. This time, the mechanism is clearer. Compliance carbon markets operate on a direct link to emissions: when industries burn more coal and heavy fuel oil as substitutes for restricted LNG, exactly what BloombergNEF analysts flagged is already happening in this conflict — their carbon liability increases. They must buy more credits. Carbon credit demand rises precisely when fossil fuel chaos strikes. That is not a coincidence. It is the architecture of the system working exactly as designed. What the Numbers Actually Say Right Now Let us get specific, because this is where the ROI case for carbon credit trading platform development becomes undeniable. The global carbon credit trading platform market was valued at $235.50 million in 2026 and is projected to reach $1.272 billion by 2034 – a CAGR of 23.47%. That trajectory was built on regulatory tailwinds alone. Now add a geopolitical multiplier that is forcing higher emissions in the short term while simultaneously making renewable energy more strategically attractive. The voluntary carbon market, which reached $1.88 billion in 2025, is expected to climb to $2.29 billion in 2026 and $4.92 billion by 2030. Even under a war economy — where corporate spending tightens temporarily — the compliance market picks up the slack. When utilities burn coal because Qatari LNG is stuck behind a military blockade at the Strait of Hormuz, they generate carbon liabilities that cannot be deferred. On European markets as of March 26, EUA carbon allowances for December 2026 were trading at €70.74 per tonne, firming upward as geopolitical tensions held. Energy market analysts noted that carbon, gas, and power prices are all now moving in lockstep with Middle East headlines. This is a structural integration that was not this visible before February 2026. The practical implication for your business: Every week of elevated oil prices is a week where carbon compliance pressure intensifies, carbon credit platform transaction volumes grow, and the window for first-mover carbon credit trading platform development narrows. Why War Paradoxically Accelerates the Green Transition – And Your Platform Opportunity Here is the mechanism that investors and enterprise strategists often underestimate. Energy pain creates energy urgency. India, currently facing a weakening rupee and rising inflation from imported oil dependency, is accelerating solar deployment not as a climate gesture but as a survival strategy. Nations that relied on Qatari LNG through the Strait of Hormuz – now functionally impaired – are stress-testing every alternative they have. That urgency does not dissipate when the conflict ends. It crystallizes into policy, infrastructure, and procurement decisions that last a decade. Each of those policy decisions generates carbon market activity. Carbon credit trading platform development sits at the infrastructure layer of all of it. Consider the compliance pathway: As countries tighten emissions frameworks in response to temporarily elevated fossil fuel use, they need digital infrastructure to manage, verify, and trade carbon credits at scale. The EU’s Carbon Border Adjustment Mechanism is expanding. India’s Carbon Credit Trading Scheme under the Bureau of Energy Efficiency is formalizing. Saudi Arabia is advancing its own Greenhouse Gas Crediting and Offsetting Mechanism. These are not distant prospects — they are live market structures being built right now, and they all require robust carbon credit trading platform development to function. Consider the voluntary pathway: ESG-driven corporates whose Q1 energy costs just jumped 20-30% are not abandoning net-zero commitments – they are looking for cost-efficient ways to meet them. A well-built carbon credit trading platform that aggregates high-quality credits, reduces broker spreads, and automates compliance reporting becomes a procurement tool, not just a sustainability checkbox. Either way, the demand side of the carbon market is expanding. The question is who owns the infrastructure that serves it. The ROI Case for Carbon Credit Trading Platform Development: Built for This Moment Let us be direct about why carbon credit trading platform development is a high-return investment in the current environment — and why that return is measurable, not aspirational. What Techaroha Builds – And Why It Matters for Your ROI Techaroha develops carbon credit trading platforms as purpose-built commercial infrastructure, not generic marketplace templates. Our implementations include smart contract-based credit issuance and retirement, AI-powered MRV verification that commands 15–25% credit price premiums, fractional tokenization for market liquidity, and real-time compliance dashboards aligned to EU ETS, CORSIA, India CCTS, and Article 6.4 frameworks. For enterprises entering carbon markets in 2026, under the pressure of $100+ oil, rising compliance obligations, and tightening regulatory frameworks, the architecture decisions made at platform inception determine whether you build a $2M compliance tool or a $20M revenue-generating infrastructure asset. The carbon market does not care whether peace negotiations succeed or fail. Compliance obligations accrue either way. Credit prices rise with geopolitical uncertainty. Transaction volume grows as more enterprises need to offset emissions they cannot yet reduce.