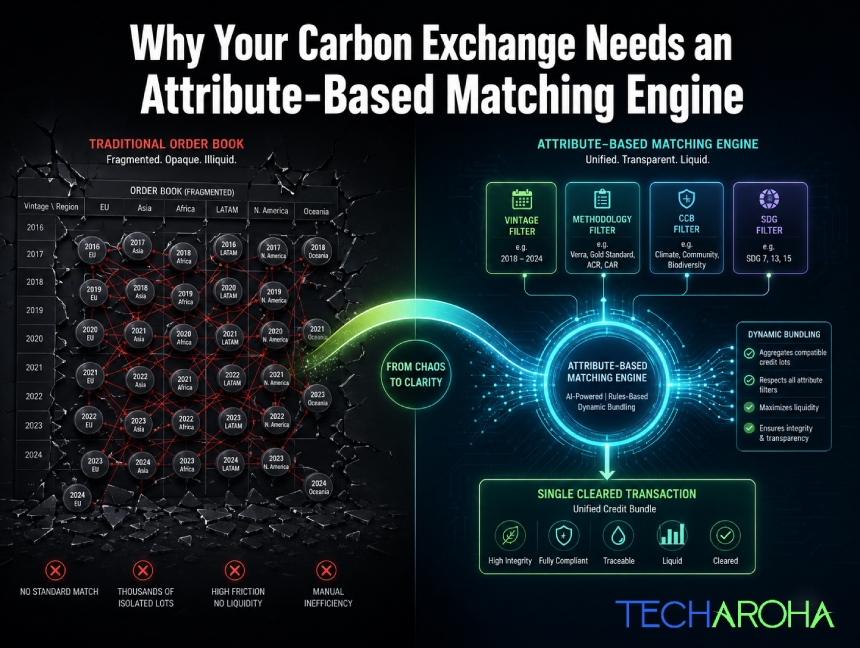

The trading infrastructure built for stocks and Bitcoin will systematically destroy liquidity in any carbon exchange. Here is the architectural fix and the exact engineering logic behind it. Carbon markets are at an inflection point. Voluntary carbon credit issuances have grown into a multi-hundred-billion-dollar projected market, institutional buyers are entering at scale, and Article 6.4 is formalizing cross-border credit flows in ways that would have seemed theoretical five years ago. Exchange founders are raising capital. Trading desks are staffing up. And almost every single one of them is about to make the same catastrophic infrastructure mistake. They are going to build a Central Limit Order Book (CLOB). The CLOB is the gold standard of financial exchange architecture. It powers the NYSE. It underpins every top-tier crypto exchange. It is fast, transparent, price-time priority-driven, and battle-tested. For carbon credits, it is the wrong tool in precisely the way that a pneumatic drill is the wrong tool for a surgical procedure. Not ineffective in general. Lethally ineffective here. This article is a precise technical and economic explanation of why, and a blueprint for the architecture that actually works: the carbon credit trading platform matching engine built on attribute-indexed, parameter-based order resolution. If you are building or operating a carbon exchange, a carbon trading desk, or evaluating infrastructure for a voluntary carbon market platform, this is the engineering decision that will determine whether your liquidity pool deepens or evaporates. Part 1: Why the CLOB Destroys Carbon Liquidity – The Structural Problem A Central Limit Order Book works on one foundational assumption: The asset is fungible. One share of AAPL is identical to every other share of AAPL. One Bitcoin is identical to every other Bitcoin. The order book can aggregate all bids and all asks into a single depth ladder because every unit on both sides of the book represents the same underlying thing. Carbon credits are not the same underlying thing. A 2021 cookstove credit from a Gold Standard-certified project in rural Kenya and a 2025 direct-air-capture credit from a Climeworks facility in Iceland are both “one tonne of CO₂ equivalent.” That is where the similarity ends.They have different: And, critically, they clear at prices that can differ by a factor of 10 or more. Institutional buyers do not treat them as interchangeable. Compliance frameworks do not treat them as interchangeable. Even voluntary corporate buyers with qualitative net-zero targets frequently cannot treat them as interchangeable without triggering greenwashing liability. What Happens When You Force Carbon Credits Into a CLOB? The matching engine identifies the asset by symbol. To maintain the fiction of fungibility across radically different credits, you have only two options: In a mature carbon market with: …you end up with thousands of discrete order books. Each one is individually empty. A liquidity pool that should be $50 million deep becomes: The consequences are predictable: The platform appears broken because, functionally, it is. This is not hypothetical. It is exactly why the voluntary carbon market spent years operating primarily as an OTC market conducted through brokers and phone calls. The asset’s heterogeneity made exchange-style infrastructure practically non-functional for real trading.A carbon credit trading platform matching engine that copies traditional financial exchange architecture without accounting for this reality will simply recreate that illiquidity problem at scale. Part 2: The Right Architecture – Attribute-Based Matching Over an Indexed Credit Graph The correct mental model for a carbon exchange is not a stock exchange. It is closer to a parametric procurement engine. The kind of system that allows a large corporate buyer to issue a single tender specification (“supply 10,000 units of this type of component, meeting these tolerances, at under this price”) and have the system dynamically identify, aggregate, and clear supply from multiple disparate sources to fulfill the single order. Applied to carbon, the architecture has three layers. Layer 1: The Credit Attribute Graph (Transactional Database) Every credit lot is stored as a structured object with a rich attribute schema not merely a quantity and price.A credit record contains: This is a normalized relational schema in your primary transactional database. PostgreSQL is an appropriate choice for ACID compliance on settlements. But the transactional database alone cannot power real-time matching at query complexity levels that carbon requires. Write about our blog that explains- The Ghost Credit Trap: What No One Tells You About Carbon Registry API Integration Layer 2: The Attribute Index (Elasticsearch or Redis Search) This is the layer many platforms either skip or implement incorrectly. The carbon credit trading platform matching engine requires a secondary search index optimized for: Elasticsearch Advantages Redis Search Advantages For institutional-scale exchanges, a hybrid architecture makes sense: Example Redis Search Schema With this index in place, the matching engine can execute parametric queries in real time. A buyer placing an order like “Buy 10,000 tonnes of any Nature-Based Removal, vintage 2023 or later, CCB certified, under $18 per tonne” translates directly to an indexed query: Example Buyer Query Buyer requests: Buy 10,000 tonnes of any Nature-Based Removal, vintage 2023+, CCB certified, under $18/tonne. This query executes against the in-memory index in under 5 milliseconds and returns every matching available lot ranked by price, regardless of which project, geography, or vintage within the buyer’s specification each lot originates from. Layer 3: The Dynamic Bundling and Clearing Algorithm The search query returns a ranked list of available lots. The matching engine’s clearing algorithm then executes a greedy fulfillment sweep: The buyer receives a single trade confirmation -10,000 tonnes cleared at a volume-weighted average price of $16.43/tonne across 7 credit lots, not 7 individual trade notifications across 7 empty order books. The seller-side experience is equally clean: individual lot holders have their available inventory consumed by the engine, with settlement proceeds routed per standard clearing logic. This is the structural breakthrough. The carbon credit trading platform matching engine does not require both sides to agree on a specific lot. It requires only that a buyer’s parameter specification encompasses the seller’s lot attributes. The parameter space is the order