The conversation around carbon markets has been dominated by one question: should we buy credits? But for platform operators – financial institutions, sustainability-focused enterprises, ESG-driven exchanges, and climate-tech founders,that is the wrong question entirely.

The right question is this: Are you positioned to own the infrastructure that others trade through?

Carbon credits are no longer an environmental checkbox. They are a maturing financial asset class with price discovery mechanisms, liquidity cycles, credit ratings, and yield curves. And like every other financial asset class in history – equities, bonds, real estate, commodities, the most durable wealth is built not by trading the asset, but by operating the exchange. Your carbon credit trading platform ROI is not found in the credits you hold. It is found in every transaction that flows through a platform you control.

This blog breaks down that financial logic, what it means for platform operators, and where the measurable return on investment actually lives.

Understanding carbon credit trading platform ROI starts with recognizing what carbon credits have become as instruments.

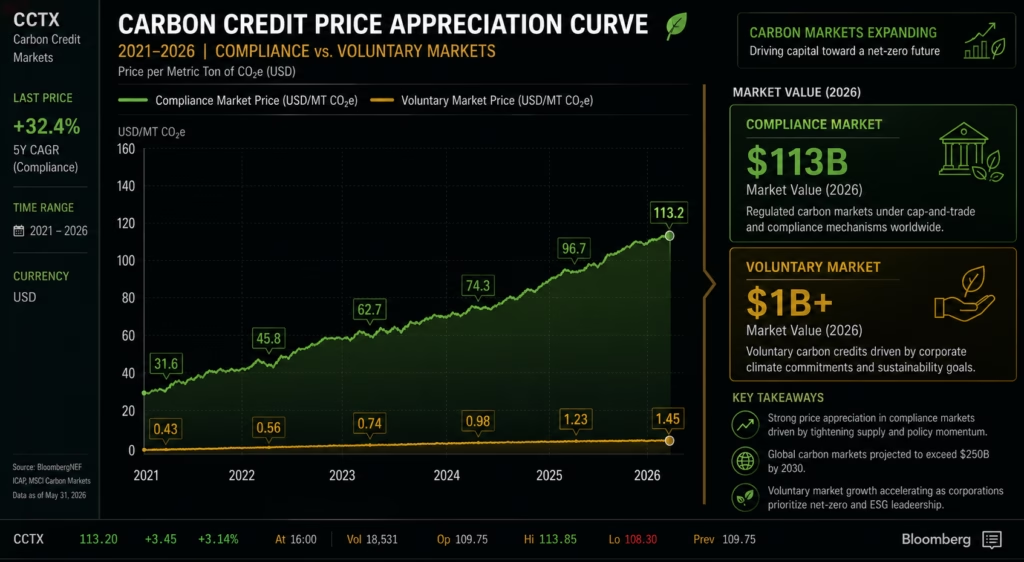

In traditional offset markets, a carbon credit was a compliance receipt proof that a tonne of CO₂ had been sequestered or avoided. Today, the picture is far more complex. High-quality nature-based credits now carry independent ratings from agencies like Sylvera and BeZero. Average spot prices for premium Afforestation, Reforestation, and Revegetation credits reached $26 per tonne in late 2025, up from $14 at the start of that year -an 86% price appreciation in twelve months. The voluntary carbon market crossed $1 billion in transaction value in 2025. Compliance markets – EU ETS, CORSIA, India’s Carbon Credit Trading Scheme are already at $113 billion and growing.

This is asset class behavior: price appreciation, quality tiering, vintage premiums, liquidity premiums, and risk-adjusted pricing. Financial instruments behave this way. Commodities behave this way. Carbon credits are now behaving this way.

For platform operators, this shift has a direct financial implication: when an underlying asset matures into a recognized financial class, the exchange infrastructure that facilitates its trading becomes extraordinarily valuable. The carbon credit trading platform ROI equation is not about holding credits, it is about owning the settlement layer.

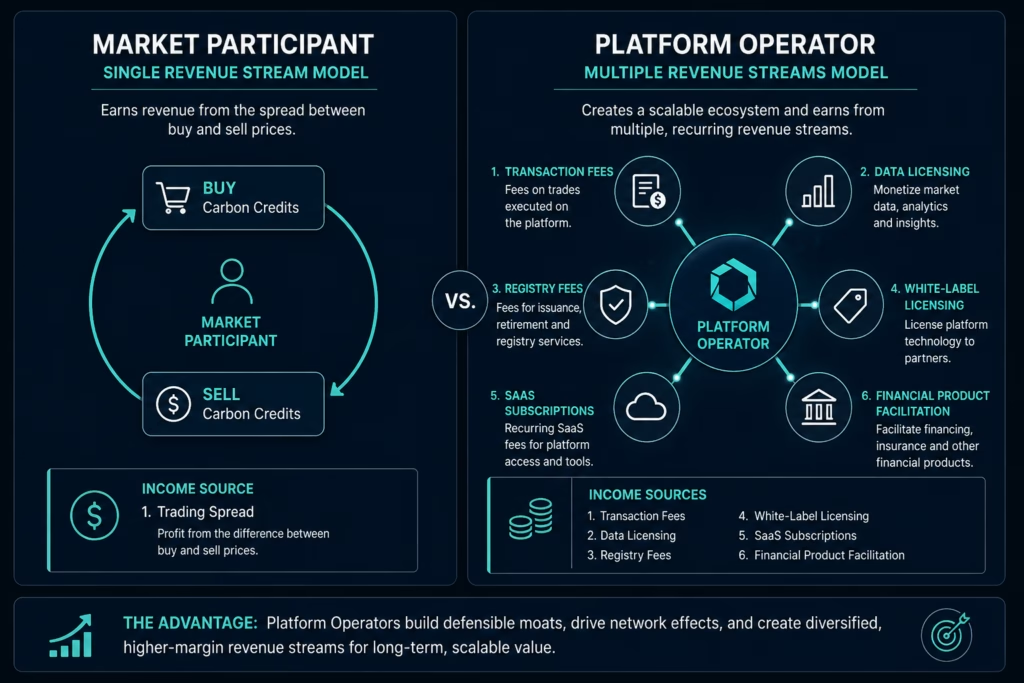

Most enterprises enter carbon markets as buyers or sellers. Platform operators enter as a third category: infrastructure owners. The distinction matters enormously to ROI.

Consider how financial infrastructure actually generates returns:

A stock exchange does not speculate on equities. It earns listing fees when new instruments come to market, transaction fees when they are traded, data licensing fees when participants need market intelligence, and connectivity fees when firms want priority access. The exchange profits whether the market rises or falls, whether individual traders win or lose. The infrastructure captures a share of every unit of economic activity that flows through it.

Carbon credit trading platforms operate on the same model. When you build and operate the exchange, your carbon credit trading platform ROI streams from six distinct sources simultaneously:

Let us put concrete numbers to this, because the carbon credit trading platform ROI case only becomes a business decision when it is quantified.

A mid-market industrial enterprise or financial institution deploying a custom carbon credit trading platform in 2026, with professional development and implementation, typically invests in the range of $150,000 to $350,000 for a production-grade system with registry integration, compliance architecture, and smart contract automation.

Year-one revenue projections for a platform processing modest volume ($30M in annual credit transaction value) at industry-standard fee structures produce $1.15M in gross revenue across transaction fees, listing fees, and basic data subscriptions. That is a 228–670% first-year ROI on the platform investment, before accounting for multi-year recurring revenue compounding.

By year three, as liquidity deepens and the platform attracts both sides of the market — project developers seeking buyers and corporates seeking verified inventory — transaction volume typically triples. White-label licensing to even two adjacent operators in related industries adds $400,000–$800,000 in high-margin recurring revenue with no proportional operating cost increase.

This is the financial logic that separates platform operators from market participants: participant ROI is linear and trade-dependent. Platform operator ROI is compounding and infrastructure-dependent.

Carbon credit trading platform ROI is not guaranteed by market growth alone. It is protected or destroyed by three foundational architecture decisions made at implementation.

Carbon markets consolidate around dominant platforms, as every maturing financial market does. The exchanges that onboard buyers and sellers first set the network effects that are structurally difficult for later entrants to overcome. CORSIA’s mandatory phase begins in 2027. India’s CCTS is live in 2026, targeting 55% of the country’s emissions. The first Article 6.4 credits are expected to reach market in 2026.

The carbon credit trading platform ROI opportunity is largest for operators who build infrastructure before the compliance wave creates institutional demand that existing platforms capture entirely.

The global carbon credit trading platform market was valued at $235 million in 2026 and is projected to reach $1.27 billion by 2034 – a CAGR of 23.47%. That trajectory was modeled on regulatory tailwinds alone. It does not include the accelerant of geopolitical energy transitions, corporate net-zero deadline pressure, or the institutional capital now flowing into carbon as an investable asset class.

Platform operators who build now are not just positioning for a compliance market. They are positioning for a financial infrastructure role in a market that is following the exact maturation path that turned commodity exchanges into multi-billion dollar businesses over the past thirty years.

Before investing in any platform, a rigorous carbon credit trading platform ROI assessment requires four inputs:

These are precisely the questions that a structured platform feasibility assessment answers — and where specialized carbon credit trading platform development and implementation partners deliver value that generic software vendors cannot.

Carbon credits are a financial asset class. The evidence is in the price curves, the quality ratings, the institutional capital flows, and the compliance frameworks forcing enterprise adoption at scale.

For platform operators, the carbon credit trading platform ROI case is not speculative. It is structural, quantifiable, and time-sensitive. The operators building exchange infrastructure in 2026 are not betting on environmental policy. They are claiming the infrastructure layer of a market that, by every historical precedent, will reward infrastructure owners disproportionately as it matures.

The question is not whether to build. The question is whether you build before your competitors do, and whether you build it right.

Ready to assess your carbon credit trading platform ROI? Our team builds and implements production-grade carbon credit trading platforms for enterprises, financial institutions, and climate-tech founders – with registry integration, smart contract compliance architecture, and launch support built in. Start your platform feasibility assessment today.